Stock Watch: Home Retail Group

Home Retail Group (LSE:HOME) owns two very well known retail chains in the form of Argos and Homebase. During the last decade the company has experienced a dramatic decline in its fortunes as the battle for shoppers has become ever more fierce. Its profitability and share price have collapsed.

Back in October the company said that things weren't going as well as it had hoped and that profits for the year to February 2016 would be lower than City analysts were expecting. This bad news led to the share price taking another lurch downwards and has left the shares looking very unloved.

So where does the company go from here?

In this article, I am going to use SharePad to look under the bonnet of Home Retail Group and see what's been going on with the company and what the future might bring.

Want to learn how to analyse shares like a professional? Download our FREE guide.

Sign-up to our mailing list to receive a PDF of our Step-by-Step Guide to Investing.

Share this article with your friends and colleagues:

Is Home Retail Group a good business?

When I begin analysing any company I start by looking for hallmarks of a quality business. My first port of call is to look at the trends in its return on capital employed (ROCE) which tells me how much profit a company is getting back as the percentage of the money it has put in. The higher this percentage, the better.

Like many people, I find it easier to understand a picture rather than wading through years of data. SharePad makes this easy by allowing you to chart loads of financial ratios over time periods of twenty years or more.

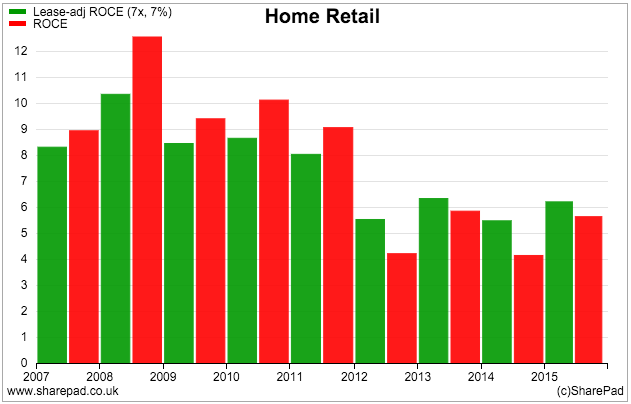

Below you can see a chart of Home Retail's ROCE over the last ten years.

I have calculated two versions of ROCE. The red bars show a standard calculation of ROCE. As you can see, this has fallen significantly from over 12% in 2009 to under 6% in 2015. This shows that Home Retail has not been a very profitable business and that its profitability is now at a very low level.

However, Home Retail is like lots of retailers in that they rent rather than own their stores. These rents (or leases as they tend to be known as) are long-term agreements and a form of hidden debt not disclosed on a company's balance sheet. This means that capital employed tends to be understated and ROCE overstated.

SharePad allows you to get round this problem by estimating the value of this hidden debt and an adjusted version of ROCE (for more on this subject click here). Whilst interest rates do change over time, I have chosen to capitalise Home Retail's rental payments (to get an estimate of the off-balance sheet debt) by multiplying them by 7 (credit rating agencies typically use a range of 6-8) and assuming an interest rate on the rents of 7%. The lease-adjusted ROCE is shown by the green bars on the chart and for most of the time has been lower than the standard version of ROCE. It is actually higher during the last three years because the interest on the leases of 7% is higher than the underlying ROCE of 6%.

All in all, whatever way you care to look at things, Home Retails ROCE is not telling me that there is a great business here - at least not at the moment.

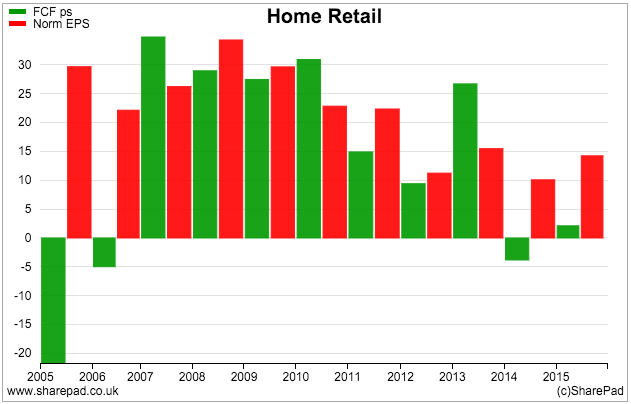

What about its ability to turn profits into free cash flow?

During the last couple of years Home Retail's free cash flow per share has been significantly less than its earnings per share (EPS). In previous years, the company's ability to turn its profits into cash has been much better, so what's changed?

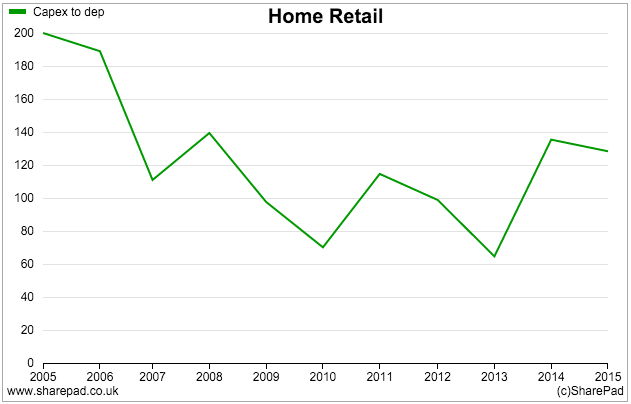

The first thing I usually look at when I come across a company with poor free cash flow is how much it has been spending on new assets (capital expenditure or capex) and compare that with its depreciation charge (an estimate of how much is needed to maintain the value of a company's existing assets). Big increases in capex reduce free cash flow.

As we can see below, Home Retail's capex spending has been going up recently and is now running at about 130% of depreciation having been below 100% back in 2013. If you go and read the company's financial reports you will learn how the company explains this rise in capex. It has been spending quite a lot of money opening up new Argos stores and converting existing stores to help with its push into internet shopping.

But is there anything else going on? On closer inspection it seems that there is.

When you are looking at a retailing company it is a good idea to pay attention to what's going on with its working capital position as it can be a big contributor to a company's free cash flow performance.

Working capital is the cash needed to run a company's day-to-day activities. Careful control of debtors, creditors and stock levels enables a company to manage the amount of working capital it requires.

Retailers need to invest cash in stock, potentially sell goods on credit (which means that sales take time to turn into cash) and have enough cash to pay suppliers (trade creditors).

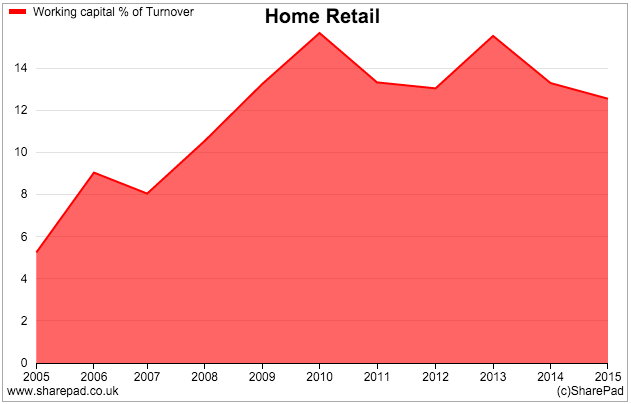

One useful ratio you can calculate is working capital as a percentage of turnover as shown in the chart below. What you can see is that Home Retail needs to invest a lot more cash into working capital than it did a few years ago and this means it cannot produce as much free cash flow.

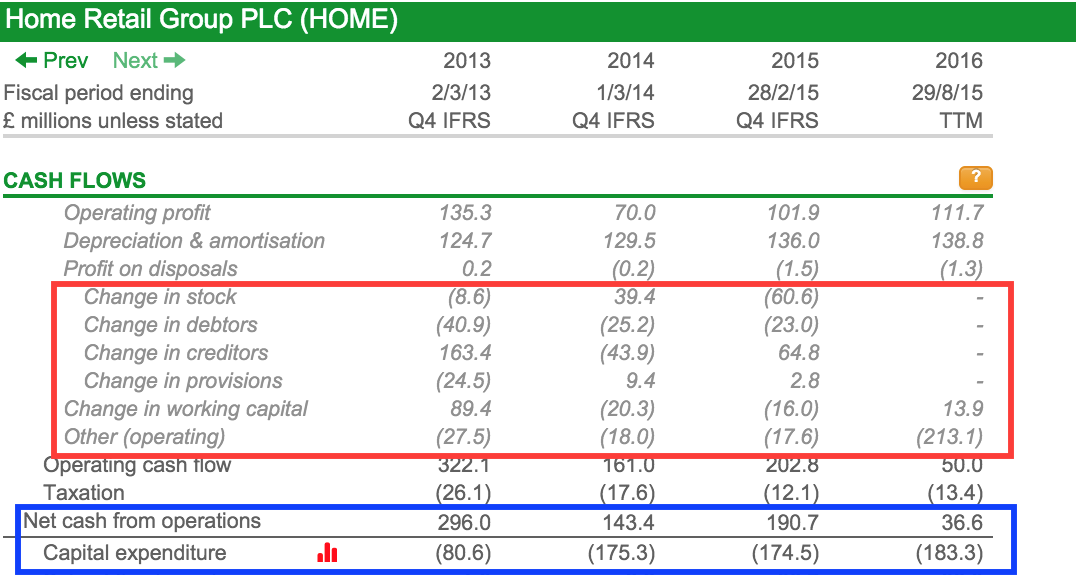

Let's take a closer look at Home Retail's cash flow statement in SharePad.

If you look inside the red box you can see how Home Retail's working capital has changed during the last three years. Back in 2013 it was getting £89.4m of cash inflow from managing its working capital which contributed to £296m of net cash from operations (trading cash flow).

In 2015, a big inflow had turned to an outflow of £16m and trading cash flow had fallen by over £100m to £190.7m. Argos has been building up its stocks of extra products in order to compete more effectively with the likes of Amazon in internet retailing. This has put a big drain on the company's trading cash flow.

If we look at the company's trailing twelve month (TTM) cash flow then it seems that things are continuing to get worse. Home Retail has produced just £36m of trading cash flow during the last year. Yet it has spent £183m on new assets (capex). The combination of building up stocks and spending on new Argos stores is eating up a lot of cash. The company doesn't have any debt but its cash balance has gone down by £140m during the last year from £333m to £193.1m. Based on what the company said in its recent half year report, this trend looks set to continue for a while yet.

So on the basis of ROCE and free cash flow, Home Retail is not looking too good at the moment.

A closer look at Argos and Homebase

If you want to learn a lot more about a company then it is a good idea to look at the breakdown of its profits in more detail. You can do this by digging into a company's annual report and finding a note in its accounts which gives you lots of extra information.

I've done this for both Argos and Homebase but will ignore the financial services business until later. Let's take a look at Argos first.

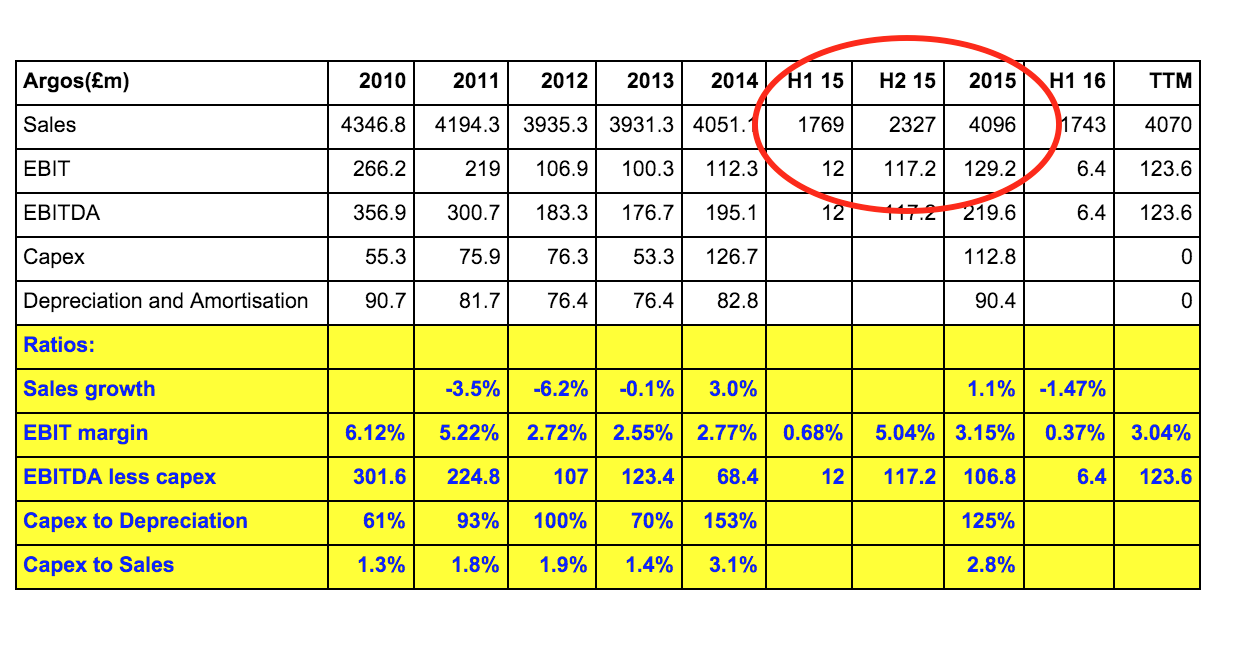

One of the most useful things you can do when you are analysing any business is to look to see if its sales and profits are seasonal or evenly spread throughout the year. You can do this by using half year (interim) and full year data to create TTM figures.

What is very interesting about Argos is that it makes virtually all of its profits in the second half of its financial year (from August to February). My guess would be that this is a business that is very dependent on Christmas shopping trends for electrical gadgets such as tablet computers and smartphones as well as toys and jewellery. This makes the business more risky. If it has a good Christmas trading period then all will be well, but if it doesn't then investors might be waking up to a nasty fall in profits when January comes around.

Argos's profits have declined from £266.2m in 2010 to £123.6m during the last twelve months. Profit margins have halved from over 6% to just over 3% now. Argos has been struggling to compete with retailers such as Amazon and John Lewis in its core products of electronics, toys and white goods (washing machines and fridge freezers). It has had to match the aggressive prices and customer service standards of its competitors and this has made the business a lot less profitable.

Argos was late in becoming an internet retailer and is now spending lots of money trying to catch up. It has recently launched a same day collection and delivery service for customers. This has meant large outlays of cash on extra products to attract customers, a fleet of delivery vans, new IT systems and extra employees.

Time will tell whether this will pay off. Amazon with its Prime service already offers a very good delivery service that is hard to compete with. However, Argos may have an ace up its sleeve given that it has over 850 stores across the UK. This may give it a competitive edge in developing a very efficient local click and collect service.

The other thing to bear in mind with Argos is that its sales and profits seem to be quite sensitive to current trends in things such as smartphones and other electrical products. A lull in new products might see its sales and profits take a dip whilst lots of new launches should be helpful.

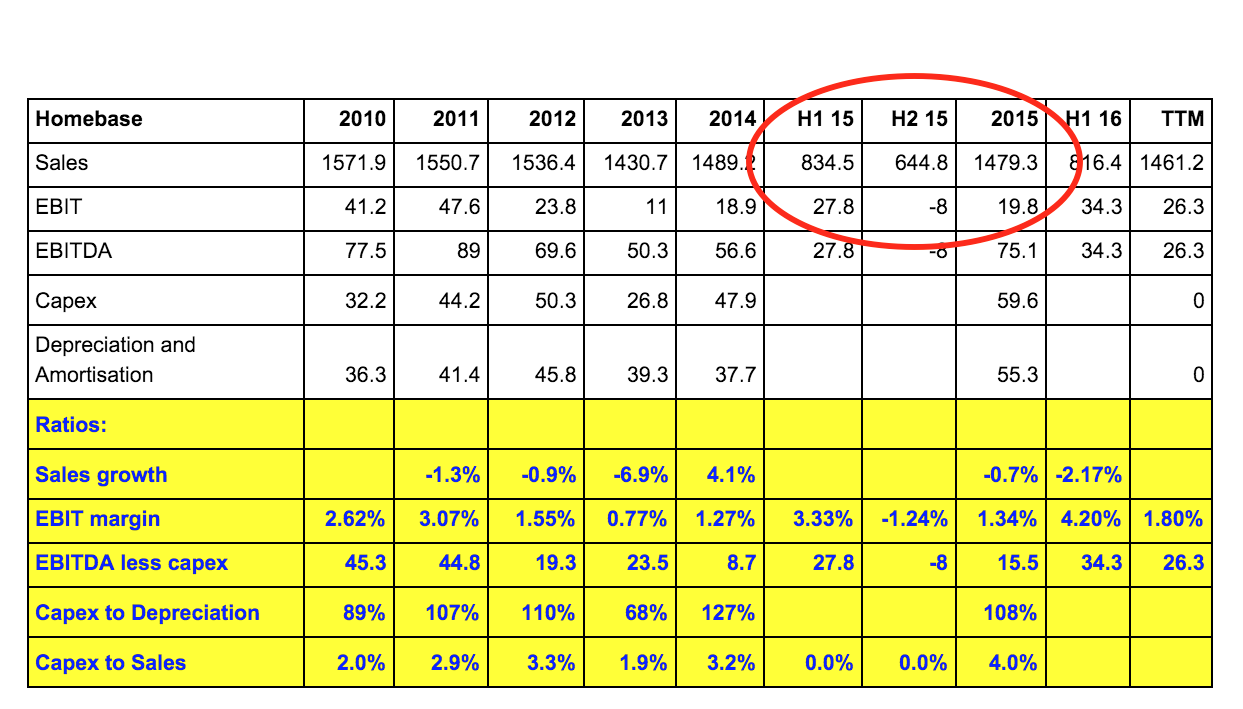

Now let's have a look at Homebase.

Like Argos, Homebase is a seasonal business. In 2015, it made all of its profits in the first half of the year (from February to August) and actually lost money during the second half of the year. The business tends to benefit from DIY, home improvements and gardening activity by its customers in the spring and the summer months.

Homebase has been a bit of a problem for Home Retail. The company is now trying to get it on an even keel by slimming down the number of stores from 323 to around 240 in a year or so. This cannot be done cheaply. Getting out of long store leases with landlords is expensive whilst selling off unsold stocks from closing stores will reduce profit margins in the short-term. The good news for shareholders is that the company is going to be able to pay for the closures with cash from a land sale in London.

After a few years of falling profits, Homebase has been able to stabilise them. It has been able to sell lots of kitchens and bathrooms to customers during the last years whilst in store brands such as Habitat have been doing well.

Yet Homebase trades on wafer-thin profit margins of less than 2% and it is difficult to see how this is going to improve in the short term. Some analysts and commentators have speculated that Home Retail might sell Homebase. After all, it makes up a very small part of total profits and is unlikely to be the main driver of the company's share price or dividend payments.

Is the company in financial difficulties?

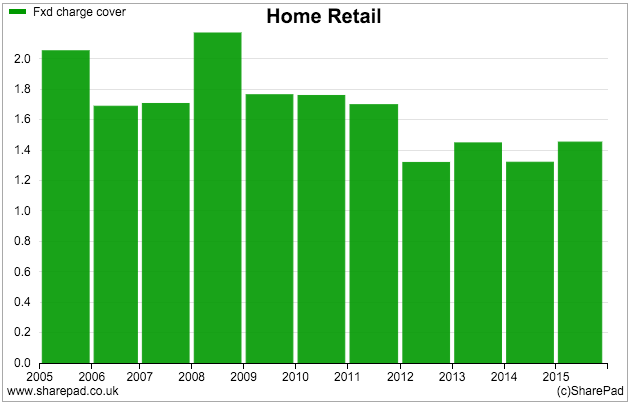

Home Retail doesn't have any debt on its balance sheet but has a lot of hidden debt in the form of the rents it has to pay on its Argos and Homebase stores. The best way to see if a retail company is heading for trouble is to calculate its fixed charge cover ratio. This looks at how many times annual trading profits (or EBIT) can cover the annual rent and interest payments (if there are any). SharePad includes the fixed charge cover ratio.

Home Retail's fixed charge cover is just over 1.4 times. That's not suggesting that the company is in the danger zone but if you are a shareholder you probably don't want to see this ratio go much lower. Anything below 1.2 would be cause for concern. You could have spotted high-profile high street casualties of the past such as Woolworths, HMV and Game Group by looking at their falls in fixed charge cover.

That said, as was shown in the cash flow statement earlier, Home Retail's trading (operating) cash flow is currently less than its trading profits (EBIT) so, on a cash basis, Home Retail's fixed charge cover has been under pressure during the last twelve months. Operating cash flow before tax on a TTM basis was £50m. In its half year results statement the company said that its rent bill for the last year was £324m. This gives you a cash-based fixed charge cover of 1.15 which doesn't look too good. How did I calculate that? Add back the £324m of rent payments to operating cash flow of £50m to get the cash before rents of £374m. Now divide this by the rental bill of £324m.

It would seem that Home Retail needs to get to work on improving its cash generation soon.

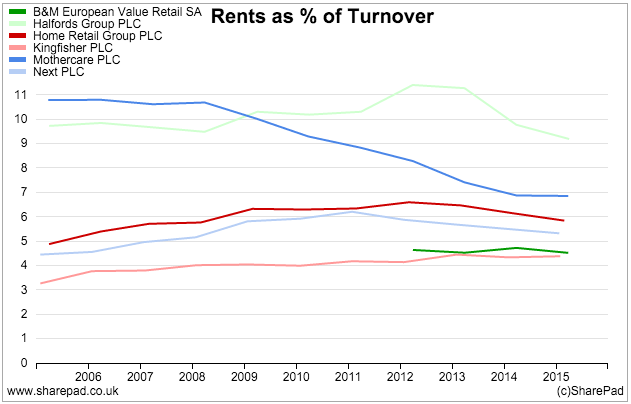

When you have a company that rents a lot of its assets as Home Retail does it can be useful to look at its rent payments as a percentage of turnover as I have done below. I've also been able to compare Home Retail with some other retailers thanks to SharePad's financial charting tool.

Around 6% of Home Retail's turnover is eaten up by rental payments. That's less than the likes of Mothercare and Halfords but is still quite a big number. It might suggest a number of things such as the company's stores may be too big for its needs, or it has expensive and uncompetitive rental agreements.

Either way, a reasonable chunk of turnover has to be paid in rents before the company makes a profit. This ratio has been falling and could keep on doing so as more Homebase stores are closed. What you can see is that Home Retail's rent costs are quite a bit more than Kingfisher's which must put it at a competitive disadvantage.

Are Home Retail shares cheap or expensive?

Home Retail's share price has taken a real battering recently. Could it be that the stock market has gone too far and pushed the shares to a level where they could be considered a bargain?

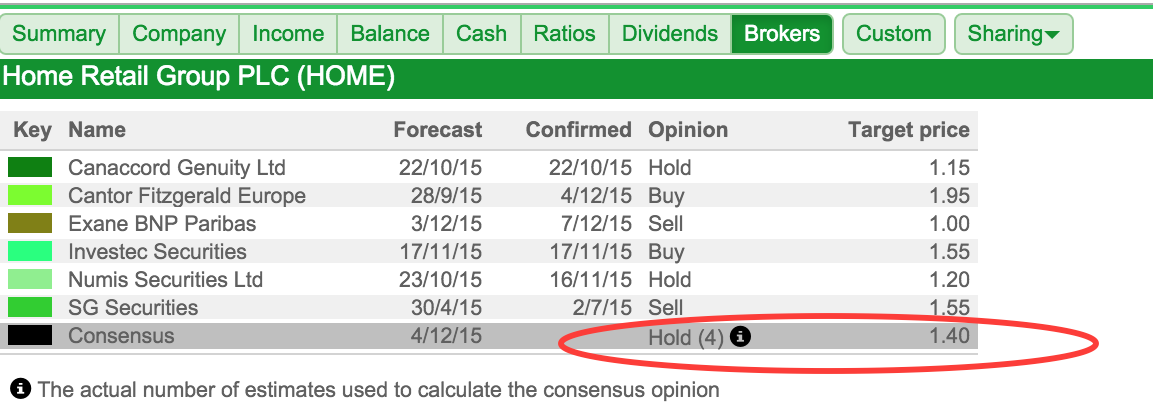

City analysts seem to think that may be the case.

The consensus share price target for the company in SharePad is 140p compared with a current share price of around 104p at the time of writing. That said, Exane BNP Paribas on 7th December seem to think that 100p is about the right price for the shares.

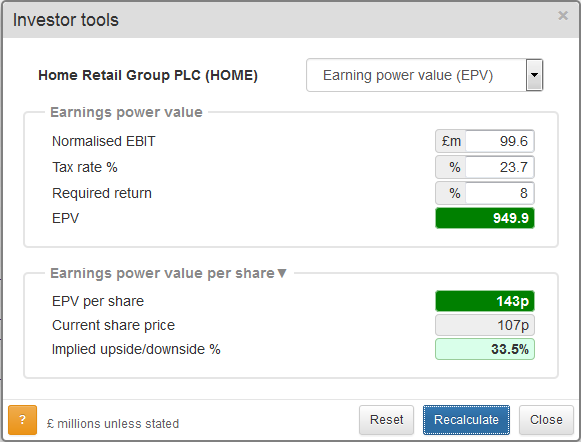

Based on forecast EBIT for the year to February 2016 of around £100m and a required return of 8%, gives an earnings power value (EPV) for the shares of 143p. To read more on earnings power values click here.

EPV's are based on a level of profits staying the same forever. But what if they don't? What if Argos's move into internet retailing and home delivery is a flop? Would you really want an 8% return to invest in the shares or would you need more than that to be tempted? If profits do fall and you want a higher return the the EPV will be lower than 143p. You can play around with the EPV tool in SharePad to test your assumptions.

You can also get SharePad to calculate some valuation multiples for a Home Retail and compare it with other retail shares as I have done in the table below.

A TTM PE ratio of 7.2 times and a lease adjusted EBIT yield (EBIT over enterprise value) of 10.1 or a price to net tangible asset value (price to NTAV) of 1.0 might make you think that the shares are cheap.

Caution is needed here. Home Retail's profits are falling and future profits are very uncertain. These valuation multiples will start to rise as profits fall - note the forecast PE is 11.2 - and make the shares look more expensive.

A low price to NTAV looks tempting. But remember NTAV ignores the hidden debts of nearly £2bn that aren't on Home Retail's balance sheet which would have to be paid off if the company was broken up and all its assets sold off.

Another approach is to do a sum-of-the-parts (SOTP) valuation which values each division of a company separately. (To read more on this valuation approach click here.)

| Home Retail plc SOTP (£m) | TTM EBIT | EBIT yield | Reason | Implied EV |

|---|---|---|---|---|

| Argos | 123.6 | 12% | EPV high interest rate to reflect falling profits | 1030 |

| Homebase | 26.3 | 10.00% | EPV high interest rate to reflect sluggish growth | 263 |

| Financial services | 1.5x estimated NAV of £48m | 72 | ||

| Central costs | -23.5 | 10% | Same forever (EPV) | -235 |

| Estimated Enterprise Values | 1130 | |||

| Adjustments: | ||||

| Net cash | 193.1 | |||

| Pension deficit | -100.5 | |||

| Provisions | -123.4 | |||

| Estimated Equity Value | 1099 | |||

| Shares in issue (m) | 813.4 | |||

| Value per share(p) | 135 | |||

The key thing to remember with this approach is that your assumptions have to be reasonable. You should try and be as conservative as possible to give yourself a buffer for being wrong.

Valuing Home Retail shares is very difficult because its future profits are so uncertain. I have valued Argos and Homebase by applying an EBIT yield to the TTM EBIT. Argos's profits are falling and will probably be a lot lower than £123m. I've no idea what they will be (a rough guess might be around £100m) but to give myself some room for being wrong I am using a fairly high EBIT yield of 12% which gives an estimated enterprise value (EV) for Argos of just over £1bn. If I thought sustainable profits would be £100m then this EV would be equivalent to an EBIT yield of around 10% (£100m/10%).

Homebase looks to be on a more even keel and so I have valued this at an EBIT yield of 10% or an EV of £263m.

Home Retail has a financial services business (a store card) to help boost sales in Argos and Homebase. After adjusting for credit that is unlikely to be paid back it has outstanding customer loans of around £550m. Once the profit from the credit has been allocated to Argos and Homebase, there is around £7m left over in profit. Home Retail targets a 15% return on equity for this business which gives an estimated book value of around £48m (48/7=15). A financial services business making these kinds of returns might be worth a price to NAV of around 1.5 times or £72m.

Central costs not allocated to Argos or Homebase are valued at an EBIT yield of 10%. After making adjustments for current levels of net cash, the pension fund deficit and provisions for things like store closure costs the estimated value per share is 135p.

If I was to base the Argos value on sustainable EBIT of £100m and an EBIT yield of 12%, Argos's estimated EV would fall to £833m and the estimated value per share would be 111p.

When you are trying to value a business it is a good idea to play around with different scenarios and see what is realistic and conservative. For example, you might want to factor in Argos's net cash balance falling if its free cash flows don't improve. Another thing to consider might be the impact of the national living wage on staff costs and profits. Alternatively you could try and value the company on the basis of higher future profits if you believe its strategy will pay off.

If you have found this article of interest, please feel free to share it with your friends and colleagues:

We welcome suggestions for future articles - please email me at analysis@sharescope.co.uk. You can also follow me on Twitter @PhilJOakley. If you'd like to know when a new article or chapter for the Step-by-Step Guide is published, send us your email address using the form at the top of the page. You don't need to be a subscriber.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.