Stock Watch: Taylor Wimpey - how to analyse housebuilders

This week I am going to be looking at housebuilding company Taylor Wimpey (LSE:TW.). Britain's housebuilders are currently enjoying a purple patch with their profits and share prices soaring. Given the tendency of Britain's housing market to swing from boom to bust and back again it's probably sensible to question whether the good times can last. Could it be that things are different this time and that share prices can keep on going up?

In this article, I'll be using ShareScope to look under the bonnet of Britain's most valuable housebuilder and also showing you some of the key areas to analyse when weighing up shares in this sector.

Want to learn how to analyse shares like a professional? Download our FREE guide.

Sign-up to our mailing list to receive a PDF of our Step-by-Step Guide to Investing.

Share this article with your friends and colleagues:

Background

The company was created in 2007 with the merger of rival builders Taylor Woodrow and George Wimpey. Its fortunes move hand in hand with the ups and downs of the housing market. It had a terrible time back in 2008 when the housing market cracked, more so than many of its peers due to the fact it had a business in the USA - where conditions were much bleaker than the UK.

Having sold off its American business, virtually all of Taylor Wimpey's profits come from the UK now but it does still have a small business in Spain.

Like most of its peers, Taylor Wimpey has had to spend a good few years cleaning itself up after the UK housing market cracked and did serious damage to its finances and balance sheet. It raised £510m from shareholders back in 2009 to get back on an even keel but had to fight very hard to restore its profits in a very tough housing market where banks - having been badly burned by the financial crisis - had been unwilling to lend people money to buy houses.

During the last couple of years, the government's Help to Buy scheme - which underwrites 20% of a mortgage loan up to a maximum property value of £600,000 - has stoked the housing market. House prices have been rising strongly and are still going up. With the banks now more confident to lend people money demand for new houses is high but the market is not being flooded with them. In short, life is currently good for Britain's builders.

What does this mean for the shares of Taylor Wimpey and other builders?

Building up a picture of a company

Before you can work out where a company is going you need to know where it has come from. The best way to do that is to study a company's financial history. This is can be done very quickly with ShareScope.

When I am researching a company for the first time, I find it invaluable to look at how it has performed in the past. By looking back at its finances over a period of at least ten years I can build up a picture of how a company has fared with the ups and downs of the economy and its industry. Once I've taken the time to do this, I feel that I am in a much better position to understand a company's current situation and what might happen to it in the future.

I am going to build up my picture of Taylor Wimpey by creating a number of results tables in ShareScope that will look at the following areas:

- Profitability - how its profits have trended in the past

- Financial strength - how strong are its finances? Have they been stable or do they move between being strong and weak?

- Cash flow - is there a good record of turning profits into cash?

- The price of the shares - how the business has been valued by the stock market in the past and whether the shares are cheap or expensive now.

I'll deal with the first three of these now but leave my analysis of the company's valuation towards the end of this article.

Profitability

Here's a results table with the key profit figures that I am interested in.

First and foremost let's look at the trend in EBIT (earnings before interest and tax) which is the company's profit from selling things. We can see that EBIT has been all over the place during the last ten years. Profits fell sharply in 2007 before moving to a position of losses in 2008 and 2009. A slow recovery then began before very strong increases in 2013 and 2014.

The fact that profits can move wildly up and down and that the company has made losses can be a sign of a very risky business unless it has changed dramatically in its make up recently. What's also interesting is that EBIT is now higher than the last peak in 2005. We need to find out if this due to a booming market or the fact that the company is just bigger. In this case, the most likely explanation is that the housing market is very favourable for builders right now.

Profit margins tell a similar story. In 2014, the company turned 18.6% of its turnover into trading profit. A much higher proportion than at any time during the last ten years. We need to find out why. For example, are its costs lower or is the company selling bigger and more expensive houses and less flats?

Capital turnover measures the amount of sales generated by a business compared with how much money it has invested (capital employed). It is a useful and often overlooked measure of how effective a company is. Back in 2005, Taylor Wimpey was producing £1.33 of sales for every £1 it had invested. Five years later, this value had collapsed to 59p but had recovered to 96p in 2014.

Capital turnover is one of the key drivers of return on capital employed (ROCE or how much profit is made per £1 invested), arguably the best way to see if a business is any good. In fact ROCE can actually be broken down into two separate components:

ROCE = operating margin x Capital turnover

In 2014, ROCE was 17.9% (which is 18.6% operating margin multiplied by 0.96 capital turnover). If you look back to 2005 when ROCE was last at a similar level, profit margins were a lot lower (12.9) but capital turnover was a lot higher (1.33).

This is important! This is telling us that how Taylor Wimpey makes its money has changed. It appears that ROCE is being driven by profit margins - which have rocketed during the last couple of years - rather than selling lots more houses. If house prices were to fall or costs to increase, profit margins could fall and ROCE could fall sharply with it. I'll have more to say on the subject of profit margins shortly.

Looking at the dividend history can tell you a lot about a company and the stability of its profits. Taylor Wimpey used to pay a much bigger dividend that it does now but stopped paying one at all in 2008 and didn't start paying one again until 2011. A company that has slashed its dividend in the past might do so again. Another thing to note is that when the company has paid a dividend, its dividend cover (the number of times earnings per share can pay the dividend per share) has always been high which may be a warning to investors that the company needs a big buffer of profits to maintain a dividend because profits can and do fall sharply when times are tough.

Taylor Wimpey's profits have been on a sharp upwards trend. Based on analysts' forecasts for EPS and dividends this is expected to continue. Forecasts always need to be treated with caution as often they are little more than a guess that a current trend will continue. Very few analysts predicted that builders would lose money in 2008 back in 2007. However, history tells us that profits can move sharply up and down in a very short space of time and will probably do so again.

Dividend forecasts also need to be carefully considered. The big increase expected from 2014 to 2015 actually reflects a special one-off dividend that is expected to be paid. Bear this in mind if you are looking for a share with a high dividend yield. Without a one-off payment the yield could be a lot smaller than its first appears to be.

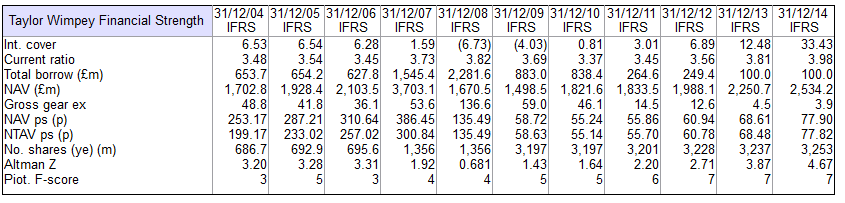

Financial strength

A business where profits can fall sharply shouldn't have lots of borrowed money. If it has any borrowings it should make sure that its profits can comfortably pay the interest owed on them. For a business like Taylor Wimpey, I'd be looking for interest cover of at least ten times - something it hasn't had until 2013. In 2014, interest cover was a very healthy 33 times which should be very reassuring for shareholders.

The company allowed itself to become saddled with way too much debt which peaked at nearly £2.3bn in 2008. This equated to 136% of shareholders' equity (net asset value) when profits collapsed and the value of the company's land had to be written down to much lower values when the housing market hit the rocks.

You can see in 2009 that the number of shares increased significantly reflecting the rights issue that took place that year. Now, Taylor Wimpey is virtually debt free, but the net asset value per share (NAVps) - a good measure of value for shareholders in this type of company - has been hammered by all those new shares. NAVps has been growing strongly recently though which is a good sign.

The Altman Z-Score is a formula used to predict which companies might be heading for financial problems. Strong companies have a score of more than 3 whilst companies with a score of 1.8 or less might be in trouble. The Z-Score signalled trouble back in 2007 but is saying that there's not a lot to worry about just now.

The Piotroski F-Score looks for companies with improving finances with good ones having a score of 7 or more. This formula would have picked up deteriorating finances back in 2006 but is telling us that all is well at the moment.

Taylor Wimpey's finances look to be in excellent shape.

Cash flow

The main thing I am looking for here is whether the company has consistently turned its profits into surplus or free cash flow. What we can see is that for most of the last decade Taylor Wimpey has produced some free cash flow. However, the record on free cash flow conversion which compares free cash flow per share with EPS is not very good. Free cash flow per share has only been more than EPS in 2007 during the last decade.

This is because the company isn't very good at generating cash from its trading activities (or operating cash flow) most of the time. This is because buying land is classified as adding to stocks or inventory which reduces cash flow. In years when the company buys lots of land this will have a detrimental effect on operating and free cash flow.

Cash return on Capital Invested (CROCI) looks at free cash flow as a percentage of money invested in the business. Because free cash flow has been patchy at best, CROCI has been low. Very good companies can have a CROCI of 15% or more, year in, year out. Even with very high profits, Taylor Wimpey's CROCI was just over 7% in 2014.

Ideally, you'd want to see Taylor Wimpey's cash performance improve from what it has been in the past.

Digging a little deeper

We've built up a picture of Taylor Wimpey. We know that its profits can move up and down a lot but are currently at a very high level. Its finances are very strong but its cash flow performance could be a lot better.

It's now time to dig into the latest company report to find out what's been going on recently and to get some kind of feel for what might happen in the future. You can access this easily in the news section in ShareScope and SharePad. It's also very worthwhile visiting the company's investor relations website (click here to go there) as there's often a lot of useful information to be found in company presentations that are given to City analysts.

Let's get started.

Taylor Wimpey's annual results announcement is packed full of useful stuff. It allows us to get behind some of the key numbers that we've been looking at in ShareScope or SharePad. Here are the key messages gleaned from it:

The management seem very confident about the future

Taylor Wimpey's management have set out some very impressive targets for the next three years (2015-17):

- A 20% average profit margin (higher than 2014)

- Return on net operating assets of at least 20% (again higher than 2014)

- To turn 65% of EBIT into operating cash flow (better again)

If it can do this then profits should continue growing strongly and cash flow should also improve which would go some way to allaying one of my concerns.

Profit per plot sold is at record levels

A breakdown of selling prices and costs per housing plot is given (basically how the company is making its money from selling houses) This is extremely useful and allows us to learn a great deal about the business when it is analysed in greater detail as I'll show below.

| Profit per plot (£k) | 2014 | 2013 | Change |

|---|---|---|---|

| Average selling price | 213 | 191 | 22 |

| Less: | |||

| Land cost | 45.1 | 41.2 | -3.9 |

| Build cost | 113 | 105 | -8 |

| Other costs | 5.3 | 5.9 | 0.6 |

| Total costs | 163.4 | 152.1 | -11.3 |

Profit per plot | 49.6 | 38.9 | 10.7 |

| margin | 0.2329 | 0.2037 | |

Plots sold | 12454 | 11696 | 6.48% |

We can see that profit per plot increased by £10,700 in 2014 to £49,600 or 23.6% of the average selling price - a record level. With the numbers above, we can see how the company achieved this.

By far the biggest contributor was the £22,000 increase in average selling prices which were achieved from a strong housing market in general and selling better quality houses. Higher selling prices were needed because the cost of building them has increased. The cost of land was higher but the company will probably be slightly worried by the increase in building costs (labour and materials) and mentioned that it is working hard to control them.

To get a proper understanding of how Taylor Wimpey's profits per building plot, I would suggest that it is worth taking the time to see if you can gather the information above for previous years. I did this by raking through company presentations on its investor website.

| Profit per plot (£k) | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|---|---|---|---|

| Avg Selling price | 188.1 | 171 | 160 | 171 | 171 | 181 | 191 | 213 |

| Less: | ||||||||

| Land cost | 46.7 | 47.5 | 34.9 | 38.1 | 35.5 | 39.4 | 41.2 | 45.1 |

| Build cost | 101.3 | 107.1 | 106.2 | 104 | 100.2 | 101.5 | 105 | 113 |

| Other costs | 16.4 | 20.1 | 7.2 | 6.5 | 6.5 | 6.4 | 5.9 | 5.3 |

| Total costs | 164.4 | 174.7 | 148.3 | 148.6 | 142.2 | 147.3 | 152.1 | 163.4 |

Profit per plot | 23.7 | -3.7 | 11.7 | 22.4 | 28.8 | 33.7 | 38.9 | 49.6 |

| margin | 0.126 | -0.0216 | 0.0731 | 0.131 | 0.1684 | 0.1862 | 0.2037 | 0.2329 |

Houses sold | 20690 | 13394 | 10186 | 9962 | 10180 | 10896 | 11696 | 12454 |

An interesting observation is that the cost per plot is almost the same as it was back in 2007 at around £164,000, yet average selling prices are £25,000 higher. Some of this will be due to the change in the quality of houses sold but I read this as an indication as to how selling prices play a key role in Taylor Wimpey's profits. This is why profits rise and fall sharply when house prices move up and down. This is the major risk you need to be aware of if you were thinking of buying some shares.

The spike in build costs in 2014 is also put into context as they have been relatively stable until then. This trend needs to be watched.

Taylor Wimpey has a very good stock of land

A large chunk of its land is in the south of England where demand for housing is high. This is likely to please investors.

Buying land at the right price is one of the key determinants of a housebuilder's profits. A buyer will work out what the selling prices of houses on the land is likely to be and all the other costs. Then they will have a target profit margin that they want to make. The missing piece of the jigsaw is the price of land. Working back from all the other numbers determines the price they will pay for the land. Getting the price right is crucial.

Taylor Wimpey says that it has been buying land that will give it profit margins of 20% at current prices which is a good sign. It also has plenty of land to build on with 75,000 plots or 6 years of work at current build rates. The company believes that this is enough and so will not be buying as much land as it has been doing in recent years. This should mean that its free cash flow should improve.

In addition to the 75,000 short-term land bank, Taylor Wimpey has 110,000 plots of what it calls strategic land. This is land that has been bought at a lower price because it does not have planning permission to build houses on. If permission is granted then the company can make more profit than if it was selling houses built on an already consented parcel of land it had bought in the past.

39% of the plots sold in 2014 came from strategic land with Taylor Wimpey looking to get this proportion over 40% in the next few years. If it can do this, then you can see how its target of 20% profit margins can be met.

The company will have to start paying tax again soon.

Although there is a tax charge of £94m in its latest accounts, Taylor Wimpey hasn't been paying much tax at all. Most of this tax charge is known as deferred tax - tax that will have to be paid at a later date on the current level of pre-tax profits.

What's been happening is that the company has been able to use the big losses that it sustained a few years ago to create tax assets. These can then be used to reduce a company's cash tax bill when it starts making profits again. The last remaining amounts of these tax assets will be used up in 2015 and so the company will have to start handing over cash to the taxman again.

Bear in mind that the company's EPS already reflects this because deferred tax has been charged against profits. However, the company's free cash flow will be reduced by the increased amounts of cash tax paid.

Taylor Wimpey is not debt free

The accounts state that the company has £112.8m of net cash (cash minus borrowings) at the end of 2014. Yet throughout the year it had an average net debt of £148.7m. It's always worth remembering that a balance sheet is a snapshot of a company's finances on one particular day. Savvy managers will usually want to show the company in its best possible light.

If you see a company with net cash on its balance sheet but with net interest payable in its income statement (as Taylor Wimpey has) then you know that the company probably has a net debt position throughout the year and might not be as financially strong as its balance sheet might have you believe.

The price of Taylor Wimpey shares

You can spend hours analysing a company, but a lot of the time spent will eventually lead you to one question: Are the shares cheap enough to buy?

As most of a housebuilders assets are in the form of land and houses being built they can be turned into cash quickly. This means that many professional investors will look to value their shares by comparing their share price to the net tangible assets per share (Price to NTAVps).

When a company is profitable and making reasonable returns on shareholders' equity (ROE) or return on capital employed (ROCE), you will usually find that its share price will be higher than its NTAVps - a price to NTAV of more than 1. When profits are low or losses are being made, the P/NTAV is low - usually a lot less than 1. Taylor Wimpey is currently trading on a P/NTAV of 2.43 which is high compared to its recent history and might be indicating that its shares are a little bit expensive at the moment. This number is certainly suggesting that the market is expecting the current good conditions to continue.

On the other hand, the PEG ratio (more on this here) which compares the PE ratio to the expected growth in EPS is less than 1 which might be saying that the shares could keep on going up.

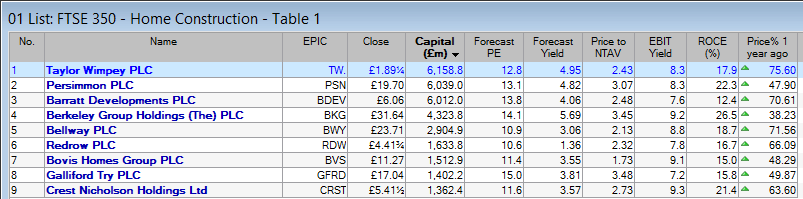

It's always a good idea to compare a company with its competitors as well. I've created a table in ShareScope below.

Taylor Wimpey has been the best performing housebuilding share over the last year with a share price gain of over 75% and is now the most valuable company in the sector.

As you can see, all the companies in the sector are making very respectable returns on capital (ROCE) and it's no surprise to see their shares trading at healthy premia to NTAV because of this. Persimmon, Berkeley Group and Galliford Try trade on more than 3 times their NTAV which looks quite expensive at first glance.

Taylor Wimpey is in the middle of the pack in terms of valuation but it seems fair to say that its shares are no bargain at current prices. However that's not to say that its shares won't continue to go up.

The table does show that Bovis Homes is the cheapest share in the sector on P/NTAV which might mean that it is worth looking at if you were thinking of investing in this sector.

If you need help creating custom Results tables in ShareScope like the ones used by Phil in this article, see page 13 of Chapter 10 - Details in the ShareScope User Manual. Alternatively, call the Support team on 020 7749 8504. We will soon be adding this facility to SharePad.

If you have found this article of interest, please feel free to share it with your friends and colleagues:

We welcome suggestions for future articles - please email me at analysis@sharescope.co.uk. You can also follow me on Twitter @PhilJOakley. If you'd like to know when a new article or chapter for the Step-by-Step Guide is published, send us your email address using the form at the top of the page. You don't need to be a subscriber.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.