Facing up to the income challenge #2: Building an income portfolio with shares

In the first part of this series on income investing I looked at how you might go about building an income portfolio with bonds (click here to read the article). Now I am turning my attention to shares. Shares have become a more popular choice for income seekers in recent years, especially in a world of low interest rates which has made it very difficult to find an adequate source of income from bonds and savings accounts.

Shares can be a great way of providing you with an income to live on. Even better than that, there is the potential to lock into an income stream that can grow over time and the prospect of seeing the value of your money invested grow as well.

However, investing in shares for their dividend income can be a risky strategy. There are plenty of traps for the unwary. Your challenge is to find enough shares to give you a high enough dividend income to live on but also where there is scope for that dividend to grow so that your income can keep up with a rising cost of living.

In this article, I am going to look at some of the ways you might try to do this and point out some potential mistakes that you should try to avoid.

Want to learn how to analyse shares like a professional? Download our FREE guide.

Sign-up to our mailing list to receive a PDF of our Step-by-Step Guide to Investing.

Share this article with your friends and colleagues:

The difference between income from bonds and income from shares

At the end of the day you might think that £1 of income from a bond portfolio is exactly the same as £1 of income from a share portfolio. In many ways it is, but how you get that income is not the same. It is important to realise that by putting your money into shares to get an income you are exposing yourself to a different set of potential risks and rewards.

With a conventional bond portfolio, unless the issuer of the bond ends up going bankrupt you know with complete certainty:

- How much income you will be paid every year.

- How much money you will get back if you own the bond until its maturity date.

This level of certainty is what attracts many people to owning bonds. However, conventional bonds (ones that pay a fixed annual income and repay the initial principal at maturity) do have a few drawbacks. The main problem is that the fixed income buys less goods and services if the cost of living is going up. The money paid back at maturity will also buy less if prices have been rising during the life of the bond.

In order to try and maintain or grow the buying power of their income and money invested, many investors have turned to shares. However, owning shares is a different proposition altogether compared with owning bonds:

- You do not know how much income you will be paid every year

- You have no idea how much money you will get back in the future.

If you own a share of a company, you are entitled to all the company's income (profit) that is left over after all its expenses and creditors (mainly interest on borrowed money, tax and preferred shareholders) have been paid. In financial jargon you have what is known as a residual claim on the company's profit - its residual income.

Some or all of this residual income might be paid to shareholders with a dividend with some reinvested back into the company to help it grow its profits in future years. The main reason for owning shares is that a company's residual income and dividend payments can grow. If that happens then the value of the share can increase as well over time. So the owner of a share - if they choose the right one - can see the buying power of their income and money invested increase (due to a rising share price) over time.

But company profits can - and frequently do - go down as well as up. If you invest in a share of a company whose profits are falling then you can often end up seeing your dividend income fall or disappear completely. This often means that the value of your investment falls as well which could leave you nursing some painful losses that you might not be able to recover from.

Last but not least, if you own shares then you must be prepared to cope emotionally with the ups and downs of the stock market. If you can't stomach seeing paper losses (losses which aren't real because you haven't sold the shares) of 20-30% or more when you open up your online broking account then investing in shares is not for you. Remember, we are talking about investing for income here and adopting a long-term strategy. As long as the company behind the shares that you own is sound and can maintain or grow its dividend then you should not worry about share prices too much.

Dividend income investing strategies

Let's take a look at some dividend investing strategies that you might consider and the main pitfalls to avoid.

Don't just buy shares with high dividend yields

It's worth reminding ourselves of what we are trying to achieve. Right at the start of the bonds article (read it here), I set out the income challenge that do-it-yourself investors are facing up to. Most of them are trying to get a better income than is available from handing their money over to an insurance company in return for a guaranteed income for the rest of their life - known as an annuity.

Here are the incomes that a £100,000 savings pot will currently buy a man just about to retire from annuity providers. Remember, anyone going down this route will - unless they buy a special type of annuity - never see their £100,000 again.

- 55 years old - £4,741 or an income percentage of 4.74%

- 60 years old - £5,181 or an income percentage of 5.18%

- 65 years old - £5,852 or an income percentage of 5.85%

So if you are looking to use a share portfolio for income instead of an annuity it might seem that all you have to do is to go out and fill your boots with shares paying a dividend yield (the dividend income per share as a percentage of the share price) of 5-6%.

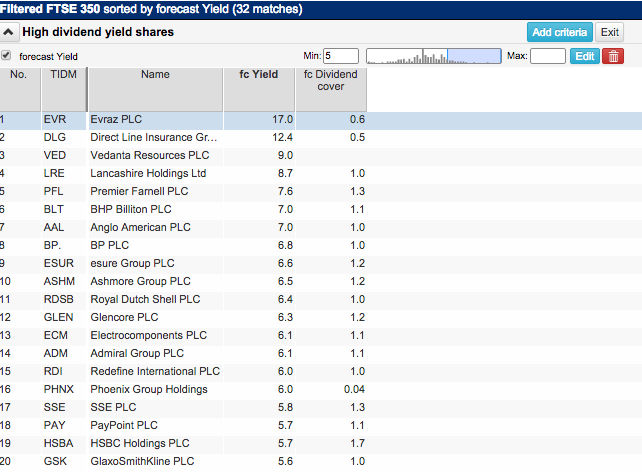

If you open up ShareScope or SharePad you can find a list of shares meeting this criteria in a matter of seconds as shown below.

In the FTSE 350 index there are currently 30 shares with a forecast dividend yield of 5%. If you were to cast your net wider and look in the FTSE All-Share index you will currently find 51 shares meeting this criteria. Many of the companies are household names. Shouldn't you just go ahead and buy 10-15 of them, sit back and wait for the income to roll in?

Not so fast. Unfortunately life is not as simple as that. If only it was. This is the kind of scattergun approach that could land you in big trouble. There are often four major problems involved with blindly buying high-dividend-yielding shares:

- The dividends aren't safe. They could be reduced or disappear entirely in the future.

- Yields can be temporarily flattered by special or one off dividends and may not be a reliable indicator of income from a share in the future.

- A portfolio has too many shares from the same area of the economy (there are six mining companies in the list above). This can mean that you aren't spreading your risks widely enough.

- The dividends are unlikely to grow much. This could mean that the income from a share portfolio might not keep pace with increases in the cost of living (inflation).

Dividends that don't look very safe

High dividend yields are often a warning sign that the dividend is not very safe and could be cut. One quick and easy way to check the safety of a dividend is to look at the dividend cover ratio. This looks at how many times the dividend per share can be paid out of current or forecast profits. You calculate it by dividing a company's earnings per share (EPS) by its dividend per share (DPS). The higher the dividend cover, the safer the dividend payout is likely to be. If a company's dividend cover is less than one (meaning that the dividend per share is bigger than the earnings per share) then its dividend is said to be uncovered.

For example a company with EPS of 100p, paying a dividend per share of 100p will have a dividend cover of 1.0 times. If you prefer, you can think about dividend cover a different way. If you reverse the calculation (divide DPS by EPS or 1 divided by the dividend cover ratio) you get what is known as the dividend payout ratio. So the company in this example is paying out 100% of its profits in dividends. If profits can't grow in the future or fall then the dividend per share will not grow or will fall.

A safer dividend is one where the company has EPS of 100p and is paying a DPS of 40p. Here the dividend cover is 2.5 times (100/40) or the payout ratio is 40% (40/100 or 1 divided by 2.5). Profits have room to fall before this 40p dividend per share is under threat.

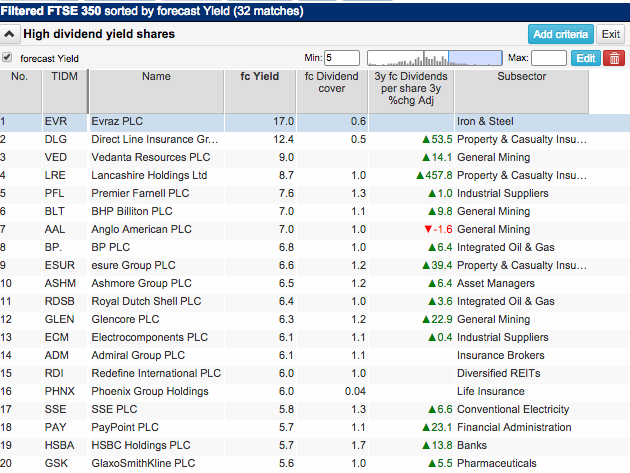

Let's take a look at our table of high yielding shares again.

What you can see is that the dividends of a lot of these very high yielding shares don't look safe at all. The dividend cover ratios are very low or not even covered at all (the dividend cover is less than one). The shares might be expected to pay out a large income during the next year but can they be relied upon to do so in later years?

The chunky dividend payouts expected from the likes of Evraz or Direct Line are essentially double the level of expected EPS and probably unrealistic or one-off payouts. This is telling you to do some digging and find out what's really going on here.

Too many eggs in too few baskets

It's a good idea when you are building a dividend income portfolio to spread your money around. Being reliant on too many shares from one sector of the economy might cause you problems if that sector hits hard times, profits fall and dividends are cut or scrapped.

It makes sense to own at least 10 and preferably 15 shares from different parts of the economy. By doing this you are spreading your sources of income around and this can help you to lower the risk that the income from your share portfolio could fall sharply in tough times.

Looking at our list of high yielding shares it is virtually impossible to spread your money around well. A large number of these shares come from depressed sectors such as mining, oil and gas and financial companies - hardly the basis of a sensible income portfolio.

Dividends that will struggle to grow

Companies with low levels of dividend cover (or high dividend payout ratios) can find it hard to grow their dividends in the future. If profits don't grow then there is little or no room to keep dividends growing. In fact dividends are more likely to fall as even a small fall in profits can make the current dividend unaffordable.

This is what seems to be the case with many of the shares in our list of high yielders. I've used SharePad to calculate the expected growth rate in dividends over the next three years as forecasted by City analysts. It is comparing the forecast dividend in three years' time with the most recent annual dividend per share.

As you can see from the list of the top twenty highest yielders, the expected growth in dividend payments is expected to be quite sluggish. Companies such as BP, SSE and Glaxo are good examples of this. Some dividends are expected to be lower. It seems that whilst you can get a high yield on some shares there is a price to be paid in terms of lower future growth or even a lower dividend income.

Some shares look more interesting at first glance but a little digging around can tell you what's going on. For example, Direct Line's very high forecast yield looks to be based on the expectation of a sizeable, one-off special dividend. Excluding this, its yield would be around 3.5%. That said, it is expected to grow its underlying dividend at a healthy rate going forward. Lancashire holdings, another insurance company, has a high yield and high dividend growth rate. But this is due to the fact that it didn't pay a special dividend in 2014 but is expected to in future years. What you need to try and avoid is buying a share with a high yield due to a special dividend that will only be paid once. When you are looking at dividend yield, always try and work out what the value of it is based on the underlying dividend - the one that is based on a company's current profits.

Also bear in mind that analyst forecasts can often be wrong and too optimistic. To be a good dividend investor, you really need to research the company and satisfy yourself that the dividend is safe and that the outlook for future profits can allow it to grow.

The risk of buying a portfolio of high yielders similar to the ones in the list above is that the income you will get from your portfolio isn't going to grow much and won't be much different from what you might get from an annuity (you do keep hold of your money though). It might therefore be worth considering a different strategy.

Trying to get the right balance between yield and growth

Given the current state of the stock market (August 2015), it appears that you will not be able to build an income portfolio with shares that will give you the same amount of income as an annuity that can grow as well - at least not to start with. You are going to have to trade off a lower initial income to start with and hope that the shares you select will grow that income over time. Hopefully, it won't be too long before your income is outpacing an annuity you could have bought today.

The trick is to get the right mix of dividend yield - it has to be sufficiently high enough to pay at least a reasonable income to start with - and dividend growth. You can do this by investing in the shares of good quality businesses. You just need to find them first.

This is when I am glad to have a copy of ShareScope or SharePad. Using the data mining feature in ShareScope or setting up a filter in SharePad, I can look for shares that could have just the right combination of yield and dividend growth.

What I have found out is that it is quite difficult to build a diversified dividend income portfolio that can do this. To me it seems that I am coming up against these issues.

- Many high dividend growers have low yields. In other words, their shares look quite expensive and there isn't enough initial income from buying the shares at current prices.

- Dividend growth with a reasonable yield is hard to come by. It is a struggle to find many shares with middling yields (3-4%) that are also capable of modest dividend growth (5-10% per year).

However, one of the best traits of good investors is an ability to be flexible and practical when faced with a few difficulties. Is it really reasonable to expect to run a single filter in a software package like ShareScope or SharePad and expect a ready-made portfolio to appear on your computer screen? Of course it isn't.

Searching for shares with filters or screens is like fishing for your supper. You might need to try fishing from different parts of the lake with different types of bait before you have enough fish to make a decent meal. With filtering, you do the same kind of thing. You try searching for shares that meet different criteria before you get enough of them that you like the look of and do some more research on them. The beauty of having a resource like SharePad or ShareScope is that your fishing need only take a few minutes once you know what you are doing.

Let me show you what I mean with a few examples.

Trawling for a dividend portfolio

There are literally endless ways to search for dividend-paying shares, but I am only going to concentrate on a few approaches right now.

As always, the shares in these filters are not share recommendations. You should always thoroughly research a share yourself before investing.

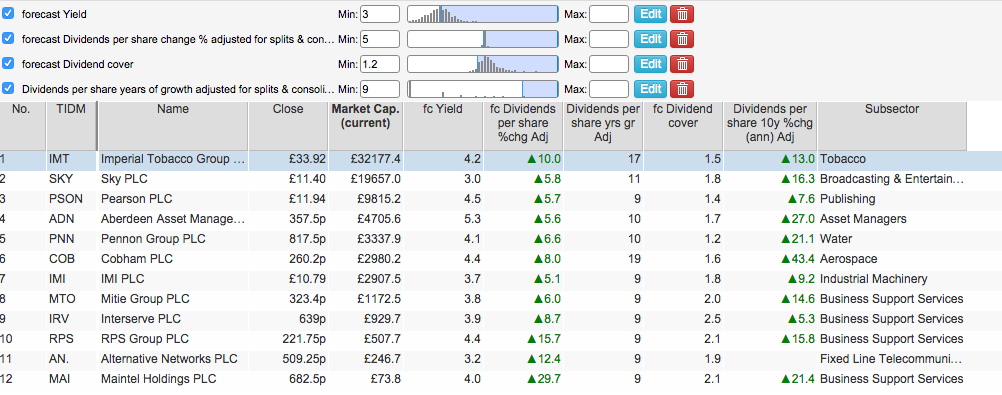

So we started out by casting our net for shares with yields of 5% or more. Now it's time to try something different. Have a look at the filter from SharePad below.

Here I am using four criteria to search for shares:

- A reasonable forecast yield of at least 4%

- Forecast dividend cover of at least 1.5 times. This might seem quite low but I don't want to exclude companies with stable profits such as utilities that can be steady and reliable dividend payers.

- Forecast dividend growth of at least 3%. This again might seem quite low but if combined with a high enough yield a share that meets this criteria might still be suitable for a portfolio.

- The company must have paid a dividend to its shareholders for at least ten consecutive years. Whilst it is not unheard of for companies with impressive dividend paying histories to suddenly slash their dividend (Tesco springs to mind here) those that have paid them for a long time have shown that they have the ability to withstand the ups and downs of the business world. This may be a sign that they can do so again and that their dividend is safer than others.

As you can see, only 16 shares meet these criteria. However, ideally we need more shares from different sectors of the economy to build a portfolio. It's time to cast the net a little bit differently.

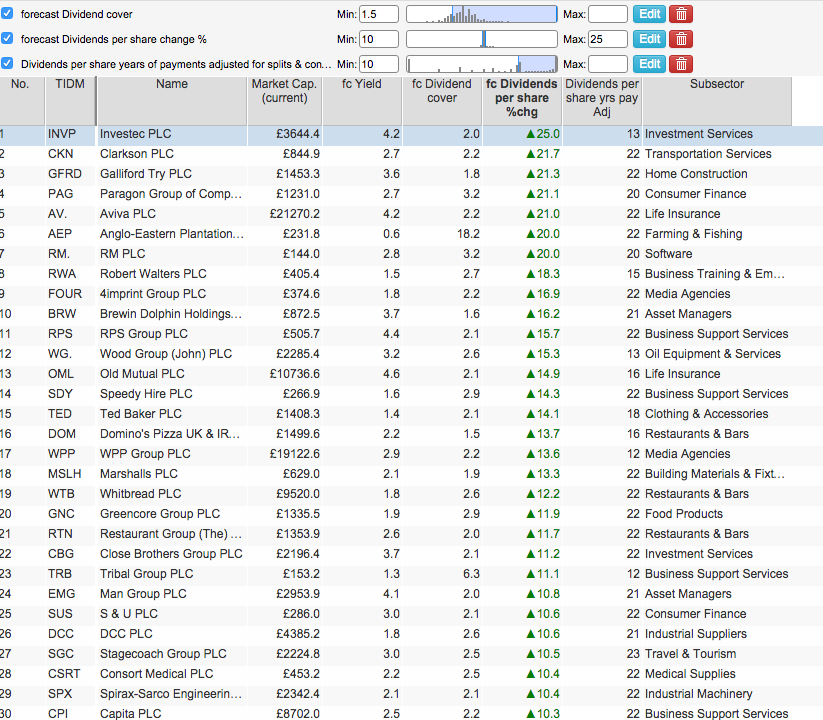

Here I've changed the criteria slightly:

- The minimum dividend yield has been reduced to 3%.

- The forecast dividend growth rate has been increased to 5%.

- The forecast dividend cover is reduced to 1.2 times.

- An historical dividend growth criteria has been introduced. I am looking for companies that have grown their dividends for at least 9 consecutive years. In other words, where dividends have been growing since at least 2005 or 2006. This means they will have kept growing their dividends through the last recession (2008-09) which could be a sign of a robust investment.

This gives a list of 12 shares to look at as shown below.

But I might want a few more shares to look at. So, I've decided to forget about dividend yield entirely and look for shares that are expected to have strong dividend growth. The criteria I have set are:

- Minimum dividend cover of 1.5 times.

- Forecast dividend growth of between 10% and 25%.

- At least ten years of continuous annual dividend payments.

This gives me a list of 35 shares, with the top 30 shown below.

An example dividend portfolio

One possibility that you could consider is to build a portfolio with different dividend characteristics with shares from different sections of the economy. So you could have a combination of:

- High yields with low growth

- Modest yields with modest growth

- Low yields with high growth

Here's an example of what you could put together and the income you might get from it. It is based on putting equal amounts of money in each share.

There are 15 different shares from 15 different sectors of the stock market. All companies are expected to be paying a higher income in three years' time than they are during the next year. The starting yield on the portfolio rises from 4.5% in year 1 to 5.1% in year 3 if current dividend forecasts are met.

Example dividend portfolio

| TIDM | Name | Price | fc Yield | fc Dividend cover | 3y fc Yield | 3y fc Dividend cover | Subsector |

|---|---|---|---|---|---|---|---|

| SSE | SSE PLC | £15.28 | 5.9 | 1.3 | 6.2 | 1.3 | Conventional Electricity |

| GSK | GlaxoSmithKline PLC | £14.19 | 5.7 | 1 | 5.9 | 1 | Pharmaceuticals |

| HSBA | HSBC Holdings PLC | 594.6p | 5.5 | 1.7 | 5.9 | 1.7 | Banks |

| AML | Amlin PLC | 522p | 5.5 | 1.5 | 5.9 | 1.5 | Property & Casualty Insurance |

| ADN | Aberdeen Asset Management PLC | 358.5p | 5.3 | 1.7 | 5.9 | 1.7 | Asset Managers |

| NG. | National Grid PLC | 855.1p | 5.1 | 1.3 | 5.4 | 1.3 | Multiutilities |

| PSON | Pearson PLC | £11.98 | 4.5 | 1.4 | 5 | 1.5 | Publishing |

| MARS | Marston's PLC | 156.2p | 4.5 | 1.8 | 5 | 1.9 | Restaurants & Bars |

| COB | Cobham PLC | 262.5p | 4.4 | 1.6 | 4.7 | 1.8 | Aerospace |

| RPS | RPS Group PLC | 226.75p | 4.3 | 2.1 | 5.7 | 1.7 | Business Support Services |

| IMT | Imperial Tobacco Group PLC | £33.71 | 4.2 | 1.5 | 5.1 | 1.5 | Tobacco |

| PNN | Pennon Group PLC | 820p | 4.1 | 1.2 | 4.7 | 1.2 | Water |

| DGE | Diageo PLC | £18.21 | 3.2 | 1.6 | 3.6 | 1.6 | Distillers & Vintners |

| SGC | Stagecoach Group PLC | 389p | 3 | 2.5 | 3.5 | 2.2 | Travel & Tourism |

| WPP | WPP Group PLC | £14.77 | 2.9 | 2.2 | 3.8 | 2 | Media Agencies |

| Portfolio | 4.5 | 5.1 | |||||

Income tomorrow rather than income today

Most of this article has been based on the task of producing a reasonable income today from a portfolio of shares. However, you might not be interested in income today but in ten or fifteen years' time when you want to retire. Would you need a different portfolio strategy to meet this objective?

Quite possibly. Instead of focusing on income producing shares you might want to focus on shares with higher growth potential to build up the value of your retirement fund so that you can turn that into more income in the future.

That's not to say that a dividend portfolio can't be a good strategy to build up your savings though. If you invest in a portfolio of high dividend paying shares, you are getting a decent chunk of your total return (the change in share price plus dividend received) from the dividend. Once that dividend has been paid, it cannot be taken away from you. A rising share price can always fall back.

But if you then use your dividend to buy more shares (known as dividend reinvestment) of the company it is possible to build up a sizeable pot of money over a long period of time (I'm talking about more than ten years here). You do this by tapping into probably the greatest wonder of the financial world. I am talking about the concept of compound interest.

With compound interest, you add any interest you receive to your initial savings or principal investment. As interest is paid on the principal, by adding interest to it the amount of interest you can earn goes up (assuming the interest stays the same or doesn't go down too much).

With shares, you use the dividend income to buy more shares which hopefully produces more dividend income to buy more shares and so on. Repeat this process for long enough and you can end up accumulating a lot more shares and a lot more income.

Let's apply this principle to our example dividend portfolio.

| Share | Share price | DPS | Shares bought | Yr 1 income | Yr 10 shares | Yr 10 income | % change |

|---|---|---|---|---|---|---|---|

| GlaxoSmithKline PLC | £14.19 | £0.81 | 423 | £342.49 | 697 | £564.46 | 64.81% |

| HSBC Holdings PLC | £5.95 | £0.33 | 1,009 | £331.99 | 1,638 | £539.04 | 62.37% |

| RPS Group PLC | £2.27 | £0.10 | 2,646 | £259.32 | 3,872 | £379.50 | 46.35% |

| Marston's PLC | £1.53 | £0.07 | 3,932 | £275.23 | 5,887 | £412.10 | 49.73% |

| Aberdeen Asset Management PLC | £3.59 | £0.19 | 1,674 | £317.99 | 2,664 | £506.13 | 59.17% |

| Amlin PLC | £5.22 | £0.29 | 1,149 | £329.89 | 1,861 | £534.03 | 61.88% |

| Stagecoach Group PLC | £3.89 | £0.12 | 1,542 | £178.92 | 2,009 | £233.08 | 30.27% |

| SSE PLC | £15.28 | £0.90 | 393 | £354.58 | 658 | £594.48 | 67.66% |

| Imperial Tobacco Group PLC | £33.71 | £1.41 | 178 | £250.79 | 257 | £362.54 | 44.56% |

| WPP Group PLC | £14.77 | £0.44 | 406 | £176.71 | 528 | £229.46 | 29.85% |

| National Grid PLC | £8.55 | £0.44 | 702 | £308.03 | 1,101 | £483.37 | 56.92% |

| Diageo PLC | £18.21 | £0.59 | 329 | £195.06 | 439 | £260.14 | 33.37% |

| Pearson PLC | £11.98 | £0.54 | 501 | £269.95 | 744 | £401.14 | 48.60% |

| Pennon Group PLC | £8.20 | £0.34 | 732 | £247.32 | 1,052 | £355.74 | 43.84% |

| Cobham PLC | £2.63 | £0.12 | 2,286 | £262.86 | 3,362 | £386.64 | 47.09% |

| Portfolio total | £4,101.12 | £6,241.87 | 52.20% | ||||

| Year 1 yield on initial cost | 4.56% | ||||||

| Year 10 yield on initial cost | 6.94% | ||||||

I am going to make a few assumptions here to keep things fairly simple.

- An investor buys £6,000 each of the fifteen shares to give an initial total investment of £90,000.

- The share prices and dividends paid do not change for ten years (this will not happen in the real world).

- The costs of buying shares (commissions and stamp duty) are ignored.

So a £6,000 investment in GlaxoSmithKline buys 423 shares (rounded up to the nearest whole number). With a dividend per share of £0.81 this gives an income of around £342 in the first year. This is then used to buy another 24 shares. And so on. After ten years, the investor ends up with 697 shares and an annual dividend income of £564 from Glaxo shares - an increase of 64% compared with the income in year 1.

Repeat this process for the whole portfolio and the annual income produced from it increases by 52% from £4101 to £6241. The value of the portfolio has also increased from £90,000 to £134,787.

All this has been achieved by reinvesting dividends with no dividend growth, no increases in share prices and no extra money added to the portfolio. If you can pick a share which delivers strong dividend growth then it is possible to make fabulous gains in wealth particularly over a long period of time. The longer you repeat the process of dividend investment, the better the results can be.

Some final thoughts

Dividend investing can be very rewarding. That said, a dividend portfolio requires regular care and attention. You should not just buy a number of shares and think that you can forget about them.

Keep an eye on your portfolio and monitor the financial performance of the companies you have invested in. If any of the shares stop meeting the criteria you have set for them or cut their dividends then you should consider selling them. You should then use the same search methods you used in the first place to find a replacement dividend paying share.

The other thing to mention is tax. The taxation of dividends is changing from April 2016. At the moment UK dividends paid to shareholders have had 10% tax taken from them (known as withholding tax) and there is no further tax to pay for basic rate taxpayers.

From April 2016, the withholding tax is being scrapped. Everyone will be entitled to receive £5,000 of dividend income per annum tax free. After that, the tax you pay depends on your other income. If you don't want to worry about the tax on the dividend income you receive then running your portfolio in an ISA is probably the best thing to do.

If you have found this article of interest, please feel free to share it with your friends and colleagues:

We welcome suggestions for future articles - please email me at analysis@sharescope.co.uk. You can also follow me on Twitter @PhilJOakley. If you'd like to know when a new article or chapter for the Step-by-Step Guide is published, send us your email address using the form at the top of the page. You don't need to be a subscriber.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.