Stock Watch: SSE - is its dividend safe?

This is week I am starting a new series of articles on analysing individual companies and their shares. I'll be looking at lots of different shares from different sectors of the stock market and will show you how you can use the information available in ShareScope - and some other bits of investment analysis - to see what kind of state a company is in.

This week's share is utility company SSE.

Want to learn how to analyse shares like a professional? Download our FREE guide.

Sign-up to our mailing list to receive a PDF of our Step-by-Step Guide to Investing.

Background information

Utility shares tend to be popular with private investors. This is based on the belief that demand for electricity, gas and water tends to be quite predictable because most of need to use it in our daily lives. This in turn can give utility companies a reasonably predictable source of income that can allow it to pay out chunky dividends to shareholders. As we shall see later, this belief could be misplaced for some utility companies.

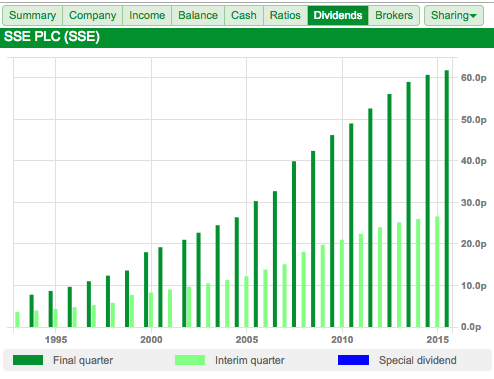

SSE has carved out a reputation as one of the most reliable dividend shares in the UK stock market. Since 1993 it has grown its annual dividend per share at an average rate of 9.8% per year from 11.4p to 88.4p. Anyone who had held the shares for this length of time and reinvested their dividends to buy more shares could have built themselves a very tidy nest egg as the share price has increased significantly as shown in the chart above.

At the current share price of 1669p, SSE shares offer a dividend yield of 5.25% based on the latest annual dividend of 88 pence per share. That's quite tempting for people looking for a good income return on their investment. What you want to know as an existing or potential shareholder in SSE is whether the company can continue to keep paying this chunky dividend and whether its shares are worth buying at the current price.

With ShareScope and SharePad you have all the information that you need to work this out - years of financial data and company reports - and I am going to show you how to use it to answer these questions.

In this analysis, I will be taking data from ShareScope and SharePad as well as information from the company's latest financial report (which you can find in the "News" section). I also tend to use spreadsheets to crunch some numbers as well but you don't have to do this.

Step 1: Understand the businesses that pay the dividend

As well as scrutinising a company's financial performance it pays to try and understand how a company makes its money. This is the first thing that I do when looking at any company. If you can't gain a reasonable understanding of this then move on to another company where you can.

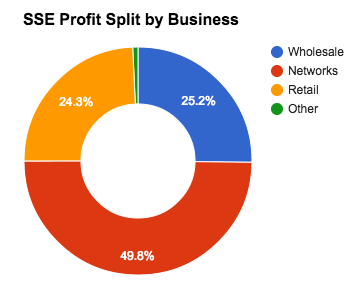

My first task is to work out how SSE's profit is made up from different businesses. You can take the numbers from the latest financial report in the News section (RNS, 20/05/15) and work this out for yourself. You do this by dividing the profit for each business by the company's total profit.

Here's what it looks like for SSE:

I can see that profits come from three main businesses. The next step is to understand what makes these businesses tick and how they have been performing. You do this by spending some time reading the company's financial reports. If you want to find out more information then a visit to the company's website is often time well spent.

This financial information is taken from the company's latest financial report. Looking at these numbers and reading what the company has to say about them is the most straightforward way of understanding a business.

| Operating profit by business (£m) | 2015 | 2014 | 2013 |

|---|---|---|---|

| Wholesale | 473.8 | 634.6 | 508.6 |

| Networks | 936.8 | 920.3 | 838.3 |

| Retail | 456.8 | 327.1 | 445 |

| Other | 14 | -1.9 | -12.9 |

| Total operating profit | 1881.4 | 1880.1 | 1779 |

The first thing to note is that total operating profits barely changed in 2015 and are not much higher than they were two years ago. That's not an encouraging sign. We need to find out what's been going on by looking at each business separately.

Wholesale (25.2% of profits)

This business has seen a sharp fall in profit. It consists of power stations that generate electricity from coal, gas and wind as well as gas fields in the North Sea and gas storage facilities. The main reason for the big fall in profit was a sharp fall in gas prices which saw North Sea profits collapse last year. Profits from power generation also fell as the company sold less electricity and cited "difficult market conditions".

Will next year be any better? Maybe. The company says that its wind farms should sell more electricity which should boost profits. However, the profits it will make from its gas and coal power stations and North Sea gas fields is a lot less certain. Long-term profits from wind farms - where SSE has been investing a lot of money - are also heavily reliant on government subsidies which could change.

What seems clear is that the profits of the Wholesale business have the potential to move up and down a lot. This may not be the kind of business that can be relied upon to support a stable and rising dividend.

Networks (49.8% of profits)

This business is doing well and is growing its profits. In simple terms it owns and looks after networks of wires, pylons and pipes which move electricity and gas from where they are produced to homes and businesses.

The amount of money that Networks can make is set by a regulator (OFGEM). In return for looking after the network assets and doing a good job for customers, SSE can be reasonably certain of how much profit it will make from this business. With extra investment in network assets, profits from this business should be very stable and continue to grow. This is exactly the kind of business that underpins SSE's dividend and it is good news for shareholders that it makes up nearly half of the company's profits.

Retail (24.3% of profits)

Selling electricity and gas to households and companies is a controversial business. The profits made by companies have been a political football in recent times. For some people, it seems that any amount of profit is unreasonable.

SSE's profits recovered this year and got back to the levels of two years ago. This was achieved by cutting costs and being more efficient. On a more worrying note, the business lost half a million customers last year. Lower gas prices are likely to reduce profits next year.

Like Wholesale, Retail seems to be a business where profits jump around a lot. It is difficult to see this business growing profits when customer numbers are falling and politicians and the media scrutinise them so closely.

To sum up, half of SSE's profits look to be in good shape. The other half is subject to much more uncertainty. That's probably not that reassuring if you want your dividend payment to keep on growing.

Step 2: Crunching some numbers

The real power of financial analysis comes with crunching numbers and calculating ratios. By doing this over a reasonable time period you can spot trends in financial performance and build up a decent picture of the company. You can then compare your picture with what the company has been saying and see if you come to the same conclusion.

This is where ShareScope and SharePad come into their own. The kind of number crunching that would take hours with a pen, paper and a calculator can be done in a matter of minutes.

When it comes to the safety of a company's dividend I am going to pay particular attention to the following bits of financial information and their trends:

- Dividend cover - how many times earnings per share (EPS) covers the annual dividend per share (DPS)

- Free cash dividend cover - is the dividend being paid out of surplus cash flow or might the company be borrowing to pay its dividend?

- The rate of capital expenditure to depreciation - how much investment spending is going on. Are the company's profits overstated? (for more on this subject click here)

- Return on capital employed (ROCE) - Are returns on investment increasing or decreasing? A falling ROCE can be a sign of a dividend that will come under pressure.

You can easily look at these ratios in SharePad. In ShareScope there is a handy little feature which allows you to create a results table with all this information in it. This is shown below.

| SSE Dividend checker | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|---|---|---|---|---|

| Dividend | 46.5 | 55 | 60.5 | 66 | 70 | 75 | 80.1 | 84.2 | 86.7 | 88.4 |

| FCF(£m) | 46.2 | 215 | 288.8 | -1370 | 527 | 482.4 | -413.6 | 181.3 | 114.2 | 249.9 |

| FCF div cover | 0.1 | 0.4 | 0.5 | -2.3 | 0.8 | 0.7 | -0.6 | 0.2 | 0.1 | 0.3 |

| CAPEX to Depn (%) | 260.1 | 201 | 298.7 | 368.7 | 248.8 | 265.6 | 330.6 | 281 | 290.2 | 242 |

| ROCE | 15.9 | 18.4 | 12.9 | 0.8 | 17.5 | 23.8 | 8 | 8.8 | 11.2 | 8.3 |

There are some interesting takeaways from these numbers:

- The dividend has been growing at a much slower rate in recent years. This may be a sign that it is getting harder to grow the dividend from profits and cash flow.

- The dividend has never been covered by free cash flow (i.e. above "1") for the last ten years. This is not a good sign but is quite common amongst utility companies.

- SSE has been investing huge amounts of money - more than twice depreciation, every year for the last ten years. Without knowing the split between stay in business capex (the cash equivalent of depreciation) and spending on new assets it is difficult to know whether profits are overstated and whether there is enough spare cash (after stay in business capex) to pay the dividend.

- ROCE is on a downwards trend. The large amount of spending on assets has not improved returns to investors.

These are worrying signs, so what has the company got to say about its dividend.

Step 3: What is the company saying about its future dividends.

Quite a lot it seems. The company's whole strategy is based on growing dividends by at least the rate of inflation in the future.

Here are some quotes from SSE's latest results statement:

"SSE believes that the quality of its operations, assets and investment opportunities means it can continue to deliver a full-year dividend that at least keeps pace with RPI inflation in 2015/16 and in the subsequent years."

This is reassuring and might be saying that all the warning signs from my analysis could be unfounded. However, there are more than a few cautious comments too.

"SSE also continues to recognise that adjusted earnings per share* is subject to significant uncertainties which mean that its dividend cover, based on dividend increases that at least keep pace with RPI inflation, could range from around 1.2 times to around 1.4 times over the three years to 2017/18. Nevertheless, SSE believes that a long-term target for dividend cover of a range around 1.5 times, also based on dividend increases which at least keep pace with RPI inflation, is the right one to aim for."

SSE is warning here that its profits could be different from what it currently expects. Dividend cover (based on profits not cash flow) could fall as low as 1.2 times which would be worryingly low. It is also saying that it is aiming for dividend cover of 1.5 times over the long haul.

This could mean lots of things. Either profits will be much higher or that dividends will increase less than profits to rebuild dividend cover. What is clear is that the current dividend and growing it by inflation to 2018 will be covered less by profits than the management wants it to be. Could this be a sign that the current dividend policy might be unsustainable?

Another thing to note is that SSE is paying a decent chunk of its dividend through issuing new shares to shareholders (known as a scrip dividend).

"The Scrip Dividend Scheme approved by SSE's shareholders in 2010 gives them the option to receive new fully paid Ordinary shares in the company in place of their cash dividend payments. It therefore reduces cash outflow and so supports the balance sheet.

The Scrip dividend take-up in August 2014, relating to the final dividend for the year to 31 March 2014, and in February 2015, relating to the interim dividend for the year to 31 March 2015, resulted in a reduction in cash dividend funding of just under GBP255.6m, with 17.1 million new ordinary shares, fully paid, being issued.

This means that the cumulative cash dividend saving or additional equity capital resulting from the introduction of SSE's Scrip Dividend Scheme now stands at GBP875.3m and has resulted in the issue of 65.9 million Ordinary shares. SSE is seeking shareholders' approval at the forthcoming Annual General Meeting to extend the Scrip Dividend Scheme from 2015 to 2018."

This has saved the company a lot of cash in recent years but the new shares will mean that future profits are spread over a bigger number of shares. But what happens when investors who are currently getting shares instead of cash decide they want paying in cash?

Step 4: How to value dividend paying shares

Here's a little bit of extra investment analysis for those of you that are interested.

One of the key questions when people are weighing up a share is how much they are worth. When it comes to dividend shares such as SSE there is a relatively simple bit of maths that you can use to work out a value based on a constant rate of future dividend growth. It is known as Gordon's Growth Model named after Professor Gordon of Toronto University who devised it.

Here the value of a share is worked out as follows:

Share Price =

Next year's dividend per share / Investor's required return minus constant rate of dividend growth

So let's try and work out a value for SSE's shares. This year's dividend is 88.4p per share. If we think that it will grow in line with inflation forever and inflation will be 2% and you want a rate of return on your investment of 8% then the implied share price is:

90.2p / (8% - 2%) = 1503p

That's less than the current share price. But what if future long term inflation is 3%? That would give a value of 1804p. What it your required return is 7% because you see SSE as a low risk investment? With 2% inflation the share price would also be 1804p.

This is a quick and relatively easy way to value a dividend share that can be done on a calculator or in a spreadsheet. The views on what returns investors should want and what the future growth will be is what professional investors spend hours trying to work out.

Remember though, that this little formula only works for companies with a constant rate of growth and won't work if the growth rate is more than the required return.

Phil Oakley