Smarter filtering for cheap shares

One of the biggest strengths of investment software like SharePad is that it allows the user to quickly search for shares that meet specific criteria - such as quality or cheapness.

It is very easy to create a screen or filter. What is more difficult is turning the information in a filter into something that actually helps you to pick a potentially winning share. The problem with filtering is that it is easy to think that investing is like painting with numbers. It isn't.

Blindly buying a selection of shares on the basis of a filter is not smart investing however appealing it might seem. It is akin to a scattergun approach and is no guarantee of making money and could be a recipe for painful losses.

In this article, I am going to use one of my favourite filters to identify potentially cheap shares. It's based on Earnings Power Value (EPV) - a valuation method often used by professional analysts. Once the basic filter has been set up, I'll show you some additional steps you can take to help you to avoid a share that might look cheap but isn't really.

Want to learn how to analyse shares like a professional? Download our FREE guide.

Sign-up to our mailing list to receive a PDF of our Step-by-Step Guide to Investing.

Share this article with your friends and colleagues:

Earnings Power Value (EPV)

EPV has its roots in the investment philosophies of legendary value investors Benjamin Graham and David Dodd. They calculated the earnings power of a company by looking at the profits of a company over a long period of time and then estimating what the average profits would be taking into account all likely business conditions.

The estimate of earnings power would then be capitalised by an appropriate factor (or multiplier such as a PE ratio) to give a prudent valuation for a company's shares. Their reasoning was that this would give them an all-important margin of safety as they wouldn't have to assume anything about the future only that it had a good chance of being similar to what had happened in the past.

You can also work out a company's EPV based on its current level of profits. If you can buy a company for a lot less than its EPV then you may have enough of a buffer or "margin of safety" to make a good profit. A share trading well above its EPV may have become too expensive - especially as any forecast growth will likely be already factored into the share price.

How Earnings Power Value (EPV) is calculated

EPV gives an estimated value for a share on the basis that a level of taxed trading profits continue forever. The concept of EPV can be a bit hard to get your head around so you can skip this section if you want. The great thing is that, if you have SharePad, the hard work is done for you.

SharePad calculates an EPV per share as shown below:

It takes the company's latest trading profit (EBIT) and taxes it at its current tax rate. It then divides the post-tax EBIT figure by an interest rate (or required return) to get an Earnings power value for the company on the basis of current trading profits staying the same forever. You could consider this EPV to be an enterprise value.

We then make adjustments for debt, cash balances, pension fund positions, preference shares and minority shareholdings to reach a value for the equity.

This equity value is divided by the number of shares outstanding to get the EPV per share.

You can then compare this with the current share price. If the EPV is above the current share price then the shares might be cheap. More often it is because the market is expecting profits to fall. However, EPV is a great help when you are trying to work out what the share price is implying about future profits.

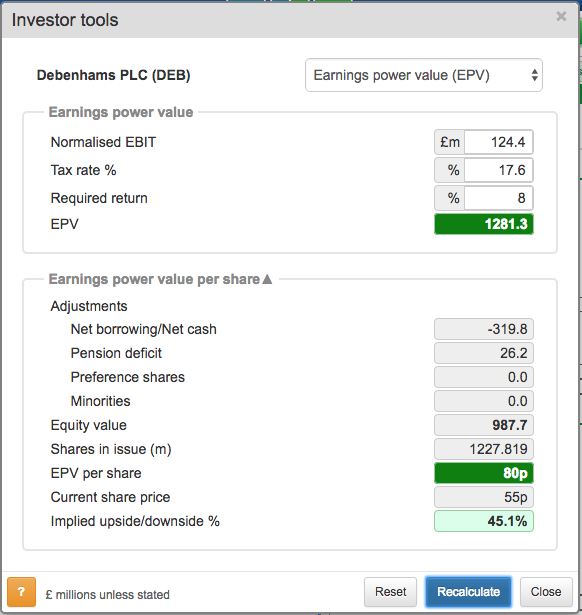

In the example above, Debenham's EPV per share is 45.1% above the current share price. Is it a bargain? Read on.

At the moment SharePad is telling me that there are just over 100 companies in the FTSE All-Share Index with share prices less than their EPV per share. Does this mean that they are all cheap?

Of course not. Many of the companies concerned will be going through tough times or are expected to. Your job as an investor is to work out whether the market has got it wrong - as it does from time to time.

Creating an EPV filter

To get the most value out of any filter, it helps to understand what the numbers behind it actually mean. By understanding and focusing your research efforts on key bits of information, you will be able to make more sense of filters and make better investment decisions, not just buying blindly on the basis of numbers.

We have seen that a company's EPV is determined by the following variables:

- Its trading profits (EBIT)

- The taxes it pays on its profits

- The interest rate required by investors - known as the discount rate or required return.

- The value of liabilities such as debts and pension fund deficits.

- The number of shares in issue.

Changes to any of the above will change a company's EPV. However, by far the most important thing to work out is the likely direction of EBIT. In most cases you want to know if it is going to stay stable or, hopefully, grow.

SharePad helps you with this. As well as looking for shares trading below their EPV value you can add an additional criteria which finds shares whose forecast EBIT is expected to be higher than the latest reported value.

If you are a SharePad user, I've included a section at the end which shows you how to add the two criteria required for this filter.

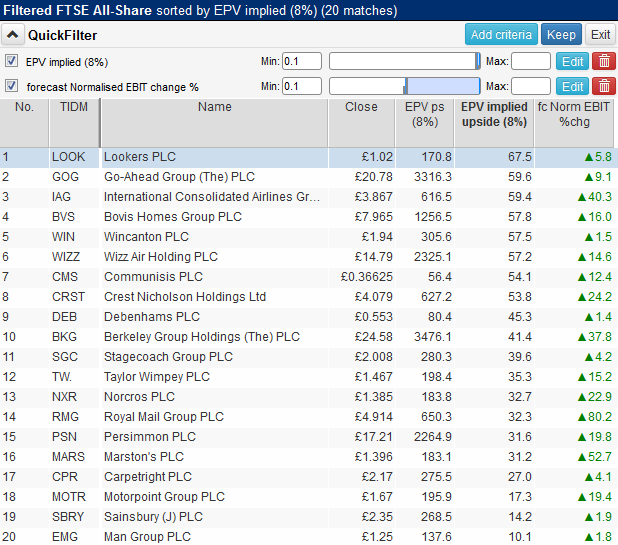

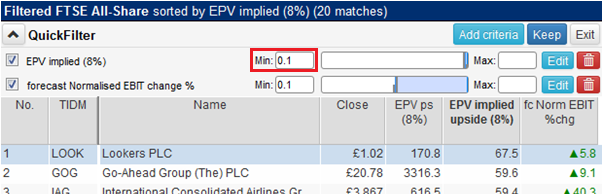

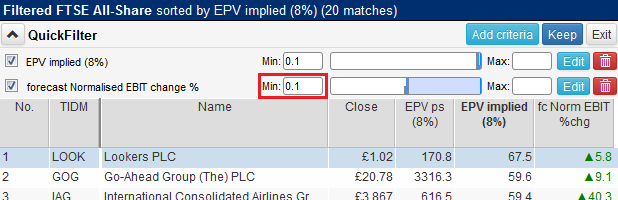

As of Wednesday 19th October 2016, the filter contains the following 20 shares from the FTSE All-Share:

As you can see, many of the companies listed above have uncertainties regarding their future profits. For example, housebuilding is historically a cyclical sector where profitability has peaks and troughs. The same can be said for airlines, retailers and car dealerships. Yet all the 20 companies listed are expected to post a higher EBIT in the next full year reporting period.

Has the stock market been too harsh? Let's take a closer look.

A case study in EPV - Debenhams

Debenhams shares have had a horrible last 12 months and have been very volatile. They were pummelled after the result of the EU referendum on 24th June, recovered slightly and have now fallen back again.

Its EPV per share based on last year's EBIT is 80p compared with a current share price of 55p.

High street retailing is fiercely competitive and it's not really surprising why anyone would question Debenhams' ability to maintain - let alone grow - its profits.

Yet despite operating in a rocky and uncertain environment, it would seem that many of the components of its EPV have remained favourable. Using SharePad forecasts and news items, I have been able to find out the following:

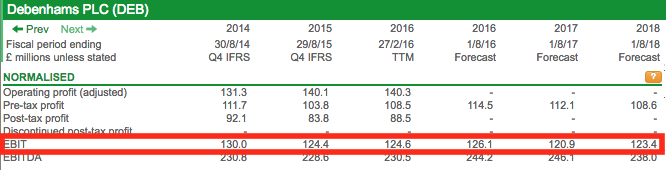

- EBIT has been maintained on a trailing twelve month (TTM) basis and is expected to be £126.1m for the year to August 2016 and relatively stable for the following two years.

- The tax rate will increase slightly to 20%. This will reduce EPV slightly.

- Net debt is expected to be £270m-£290m compared with £319m last year. This will increase EPV.

- The pension fund surplus increased from £26.2m to £51.8m in February, but it is possible that this could have turned into a deficit given, low interest rates and what has happened to other companies' pension fund deficits recently (Note: Tesco's increased by £4bn to over £7bn between February and August 2016)

According to a news story on SharePad, analysts at Morgan Stanley think that Debenhams could have a pension fund deficit of more than £200m.

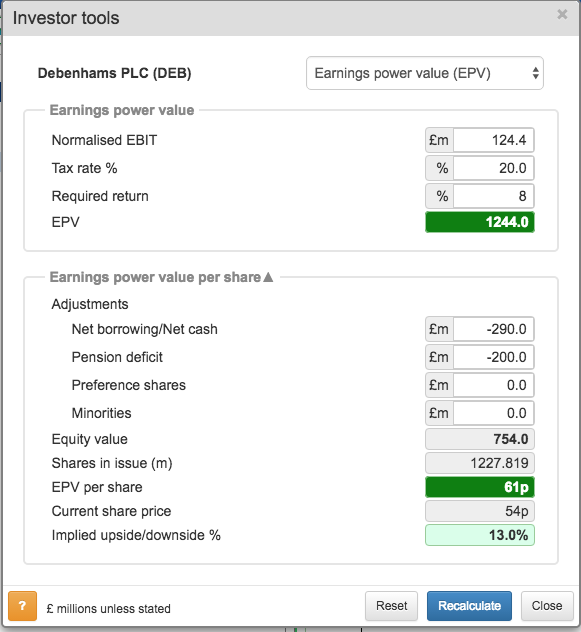

We can put this up-to-date information into SharePad's EPV calculator to come up with a new estimate of EPV per share:

The new EPS per share of 61.4p for Debenhams suggests that the shares are not as cheap as previously thought.

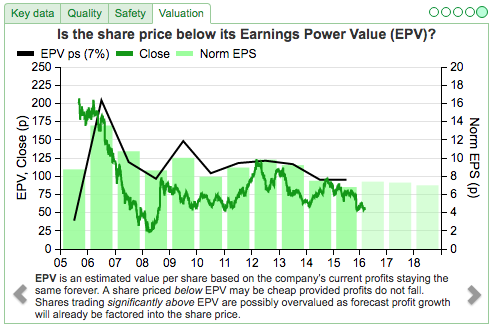

Charting EPV

I'd like to highlight the new financial charts carousel in SharePad if you haven't already seen it. You'll find the carousel on the Summary tab of the Financials view (below the Dashboard and Momentum chart). You can see a screenshot below for Debenham's.

The final chart on the Valuation tab of the carousel (shown above) shows you the relationship between the share price, the EPV per share and future profits.

We've used Normalised EPS here as a proxy for Normalised EBIT because not all companies have a forecast EBIT value - particularly smaller companies - whereas most have forecast EPS.

To sum up

A share may be cheap:

- If trading below its EPV and profits are forecast to grow.

- It may also be cheap if trading significantly below EPV and profits are forecast to remain stable.

- Try calculating EPV using forecast EBIT.

- Use interim announcements to check if liabilities are expected to increase as these can reduce the EPV. Include these in your EPV calculation.

A share may be expensive:

- If trading above its EPV and profits are forecast to remain stable or even fall.

- If trading significantly above EPV and profits are forecast to grow strongly (as this may already be reflected in the share price). For example, a fast growing company with its shares trading for more than twice its EPV might be considered expensive.

- Try calculating EPV using forecast EBIT.

- Use interim announcements to check if liabilities are expected to decrease as these can increase the EPV. Include these in your EPV calculation.

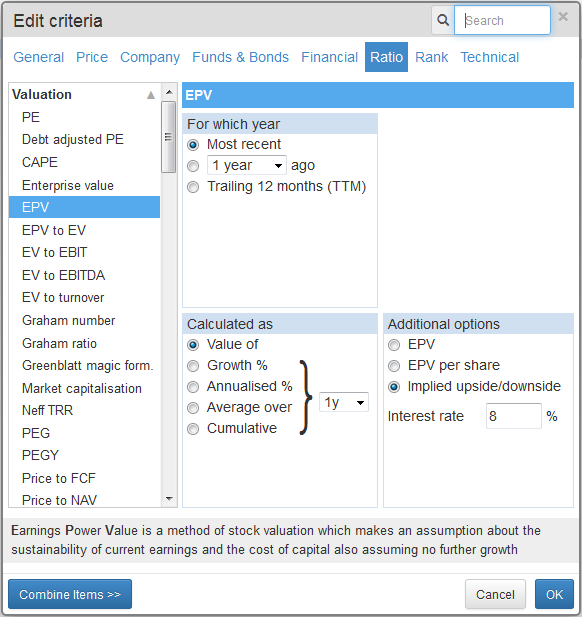

Creating the EPV filter

When you add a criterion to your filter, select EPV on the Ratios tab (see screenshot below). I've set the Interest rate to 8%. I've also selected the option called Implied upside/downside. This tells you how far above or below the current share price the EPV per share is.

Remember, we want shares where the EPV is above the share price (i.e. there is a potential upside to the share price), so when you've added the criteria, set the minimum upside/downside to 0.1 as in the screenshot below.

Note: you may find this EPV Upside/downside useful as a column in your portfolio table.

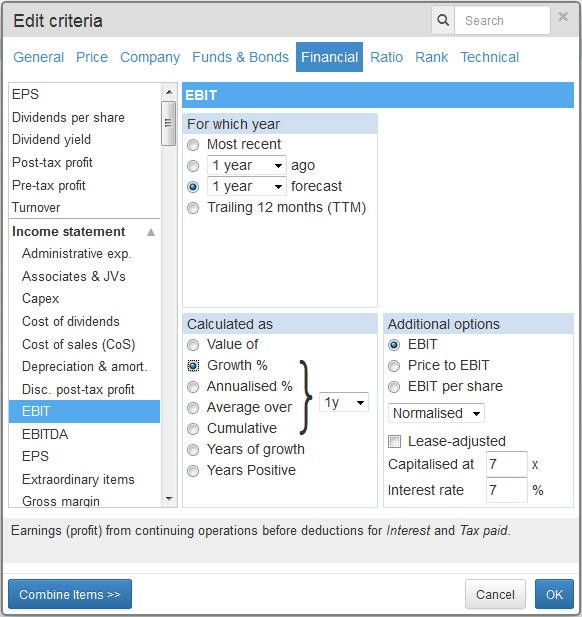

To add the criteria for EBIT growth, select EBIT on the Financial tab as shown below. Make sure you select the options for 1 year forecast, Growth % and Normalised.

As we only want companies with increasing profits, set the minimum value for forecast EBIT growth to 0.1 as shown below.

If you have found this article of interest, please feel free to share it with your friends and colleagues:

We welcome suggestions for future articles - please email me at analysis@sharescope.co.uk. You can also follow me on Twitter @PhilJOakley. If you'd like to know when a new article or chapter for the Step-by-Step Guide is published, send us your email address using the form at the top of the page. You don't need to be a subscriber.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.